The future outlook for the banking sector in Poland is positive. Key banking volumes are expected to accelerate in 2014-2015. However, the growth in banks' revenues and profits might temporarily be held back by a number of factors including: unfavorable regulatory developments (e.g. card interchange), increasing risk costs and higher operating expenses.

Poland's banking market continued to consolidate in 2013. Bank PKO took over most of businesses of Nordea Group in Poland, including Nordea Bank Polska, BNP Paribas agreed to buy BGZ bank and Getin Noble acquired retail operations of DZ Bank. However, the appetite for consolidation met growing resistance from the regulator: KNF (Polish Financial Supervision Authority). In recent statements, KNF described current level of concentration in the banking sector as "close to optimal" and warned that further mergers would be thoroughly examined (which means that further M&A is unwelcome).

For more information on recent developments in the Polish banking sector, please refer to the full publication.

Table of contents

Slide 1: Executive summary

1. Macroeconomic overview Slide 2: Poland - General overview

Slide 3: Key macroeconomic indicators, 2007-2013

Slide 4: Foreign trade statistics, C/A balance, FDIs, 2007-2013

Slide 5: Unemployment and salaries, 2007-2013

Slide 6: Disposable income in households, 2007-2013; income distribution 2012

Slide 7: Consumer confidence Index evolution, 2009-1Q/2014

Slide 8: Warsaw Stock Exchange - Turnover, Market cap and indexes, 2007-2013

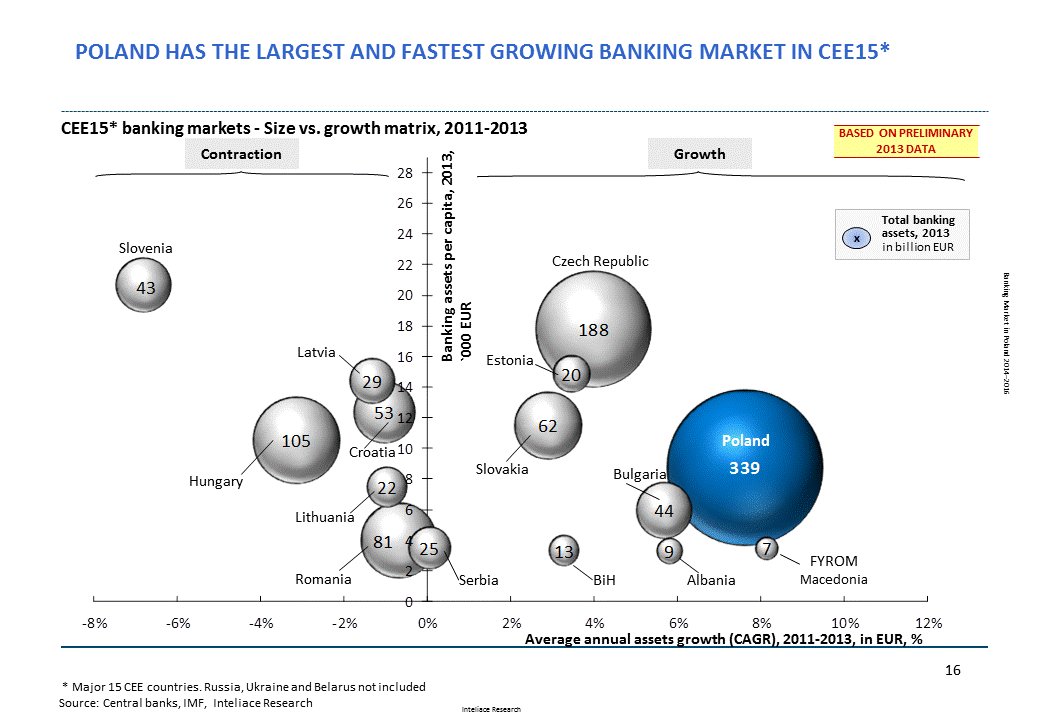

2.1. Banking market - General trends Slide 9: CEE banking markets: Size vs. growth matrix, 2011-2013

Slide 10: CEE banking penetration benchmarks - International comparison, 2013

Slide 11: Structure of the Polish Banking System, 2013

Slide 12: Polish Banking System ERA analysis, 1989-2013

Slide 13: Evolution of banking assets by groups of owners (domestic/foreign), 2002-2013

Slide 14: Top 10 foreign investors in the Polish banking market, 2013

Slide 15: Banking assets evolution (LCU, EUR), 2007-2013

Slide 16: Banking assets evolution by groups of banks, 2007-2013

Slide 17: Top 12 commercial banks, market shares, ownership, 2013

Slide 18: Evolution of market shares for top 8 commercial banks, 2011-2013

Slide 19: Concentration of the banking market, 2012 /2013 (Assets, Branches, ATMs, HH Index)

Slide 20: Deposits by customer segment evolution, 2007-2013

Slide 21: Loans by customer segment evolution, 2007-2013

Slide 22: Foreign funding evolution, 2007-2013

Slide 23: Non-performing loans value and NPL ratios by type of business segment, 2009-Feb.2014

Slide 24: Non-performing retail loans, ratios by type of product, 2005-2013

2.2. Banking market - Regulatory overview Slide 25: Regulatory overview: Regulatory bodies in the Polish banking market

Slide 26: BFG - Deposit Insurance Fund

Slide 27: BIK - Credit information Bureau

Slide 28: BIG - Regulated commercial/consumer information providers

Slide 29: Central Bank interest rates and mandatory reserve policy, 2000-2013

Slide 30: Inter-bank yield curves, 2010-2013 (WIBOR 3M, Polonia O/N)

Slide 31: Basel II/CRD implementation status, Capital requirement, own funds and CAR ratio for banks, 2009-2013

Slide 32: Consumer and mortgage lending-regulatory changes

Slide 33: New taxation initiatives affecting banking sector in Poland, 2013

2.3. Banking market - Banking Infrastructure Slide 34: Bank outlets by type of bank, 2008-2013

Slide 35: Employment in commercial banks, bank assets per employee evolution, 2008-2013

Slide 36: Direct employee costs evolution, 2009-2013

Slide 37: ATM number and transaction value evolution 2008-2013, ATM players, 2013

Slide 38: POS number and transaction value evolution 2008-2013, POS players, 2012

3. Retail banking Slide 39: Demographic trends determining future number of bank clients, 2007-2020F

Slide 40: Demographic and social trends influencing future number of bank accounts

Slide 41: Retail banking clients by segment - pyramid (mass market, affluent, personal and private banking), 2013

Slide 42: Households deposits by sub-segments, 2007-2013

Slide 43: Cash in circulation, cash vs. deposits ratio, 2007-2013

Slide 44: Household loans by sub-segments evolution, 2007-2013

Slide 45: TOP banks serving households sector, market shares, 2012

Slide 46: Deposits of private individuals, structure by currency, 2007-2013

Slide 47: Deposits of private individuals, structure by maturity, 2007-2013

Slide 48: Current account penetration in Poland, Bank account holders demography, 2012

Slide 49: Current accounts of individuals (ROR) at major banks, 2011-2013

Slide 50: Internet and PC penetration in Polish households and in corporate sector, shopping online, 2013

Slide 51: Number of accounts with online access and number of online accounts actively used, 2008-2013

Slide 52: Online Banking - mBank case, 2001-2012 (discontinued)

Slide 53: Online Banking - new entrants: ING and Citibank and perspectives for standalone internet projects

Slide 54: Mobile Banking - availability of mobile account access , overview of top 10 banks

Slide 55: Mobile Banking - concepts of the future: Alior Sync (t-mobile usługi bankowe) , new mBank

Slide 56: Innovation in payments-PKO IKO, PeoPay, iKasa, SkyCash, mPay, Orange Cash, T-mobile , MyWallet , Visa V.me

Slide 57: Bill payments market structure, 2012 (discontinued)

Slide 58: Investment funds assets evolution, domestic and foreign funds, 2007-2013

Slide 59: Investment funds - top 10 players, 2013

Slide 60: Personal Financial Assets (PFA) structure and evolution, 2010-2013

Slide 61: Loans to private individuals by type evolution, 2007-2013

Slide 62: Mortgage to private individuals by currency evolution, 2007-2013

Slide 63: Mortgage to private individuals-new sales, outstanding contracts, 2007-2013

Slide 64: Consumer lending market, volumes and values, 2010-2013

Slide 65: Loans penetration in Poland vs. EU, EUROBAROMETER 2008/2009

Slide 66: Dedicated car loans market, 2009-2012

Slide 67: Value and number of loans and investment products sold by major intermediaries, 2012

3.1. Payment cards Slide 68: Cards issued by type, 2008-2013

Slide 69: Card transactions by type (cashless, cash), share of cash transactions, 2008-2013

Slide 70: Credit card transactions , values, volumes, per card evolution, 2008-2013

Slide 71: Top players in credit cards business, co-branding partners, 2013

4. Corporate banking Slide 72: Corporate subjects by size, number, employment, revenues and profits, 2012

Slide 73: Corporate subjects, revenue and profit evolution, 2008-2013

Slide 74: Corporate subjects, regional distribution, 2013

Slide 75: Corporate deposits and loans evolution, 2007-2013

Slide 76: Top players in the corporate banking market, 2013

Slide 77: Brokerage business, top players, shares of investors groups, 2008-2013

Slide 78: Leasing market, structure by industry, top players, 2008-2013

Slide 79: Factoring market, 2008-2013

Slide 80: Non-treasury debt securities market, 2008-2012

5. Banks' profitability Slide 81: Nominal rates on loans and deposits by segment, implied margins, 2010-Feb.2014

Slide 82: Commercial banks - profitability tree, 2010-2013

Slide 83: Commercial banks - revenue, costs and profits composition, 2013

Slide 84: Commercial banks - revenue, costs and profits composition, 2012

Slide 85: Top 5 commercial banks profitability tree-peers comparison, 2013

Slide 86: Segment reporting (1/2): volumes, revenues and profit by segment (retail, corporate, other), 2013

Slide 87: Segment reporting (2/2): volumes, revenues and profit by segment (retail, corporate, other), 2013

6. Banks' valuation and M&A activity Slide 88: Share price performance in the stock market for key listed banks in Poland, 2012/2014

Slide 89: Market multiples for major listed banks in Poland, 3/2014

Slide 90: Strategic control map for major listed banks in Poland, 3/2014

Slide 91: Efficiency of top banks in Poland - Cost to income, Assets/Personnel/Branches benchmarks, 12/2013

Slide 92: Acquisition transactions in the Polish banking market (1/3), 2005-2008

Slide 93: Acquisition transactions in the Polish banking market (2/3), 2009-2011

Slide 94: Acquisition transactions in the Polish banking market (3/3), 2011-2013

Slide 95: New entrants, 2013/2014

Slide 96: Mergers in the Polish banking market, 2009-2013

7. Top 5 banks - Profiles Slide 97-98: Bank profiles: PKO Bank Polski

Slide 99-100: Bank profiles: Bank Pekao

Slide 101-102: Bank profiles: mBank

Slide 103-104 Bank profiles: ING Bank Śląski

Slide 105-106: Bank profiles: BZ WBK

8. Mid-term forecasts Slide 107: Banking assets forecast, 2013-2015

Slide 108: Key retail volumes forecast, 2013-2015

Slide 109: Key corporate volumes forecast, 2013-2015

9. Notes on methodology

Research Report: "Banking market in Poland, 2014-2016"

Research Report: "Banking market in Poland, 2014-2016"