Turkey's economy grew at a 3.3 percent annual rate in the first half of 2014 despite increasing global economic headwinds. Key banking volumes reflected the robust economy, however, growing at decelerating rates. Total assets increased to a record TRY 1.65 trillion (EUR 631 billion) as of June 2014. Lending remained relatively strong (+5% growth in value of outstanding loans during Jan.-Jun.2014), despite growing interest rates. The weakest segments were car and credit card lending hit by regulatory actions and by growing unemployment. Total deposits increased only by a fraction during H1 2014, driven up mostly by retail volumes.

In terms of profits, banks were able to post solid results in H1 2014. Despite gradually falling (since 2012) interest margins and stagnating fee & commission income, banks managed to produce higher profits thanks to growing underlying volumes. A closer look at P&L statements of the banking sector in H1 2014 points to a good control of operating costs and a falling impact of bad-loan provisions (on a relative basis vs. total assets). The NPL* ratios for commercial loans and housing loans keep falling, however, credit card debt and other consumer lending showed first signs of deterioration, which could be attributed to higher interest rates and growing unemployment.

For more information on recent developments in the Turkey's banking sector, please refer to the full publication.

Table of contents

Slide 1: Executive summary

1. Macroeconomic overview Slide 2: Turkey - General overview and key facts

Slide 3: Selected macroeconomic indicators, 2010-2014 H1

Slide 4: Foreign trade statistics, C/A balance, FDIs, 2010-2014 H1

Slide 5: Public finances, 2010-2014 H1

Slide 6: Disposable income in households, 2009-2013; income distribution 2013

Slide 7: Borsa Istanbul- Market cap , # equities, index, 2009-Sep. 2014

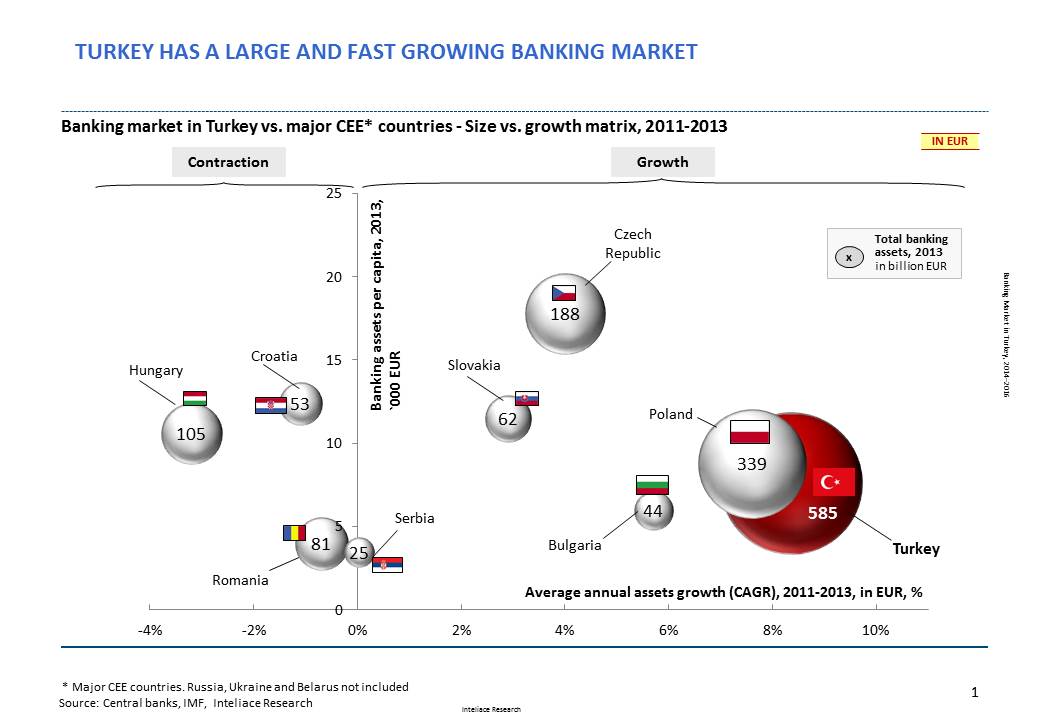

2. Banking market Slide 8: Turkey and CEE banking markets: Size vs. growth matrix, 2011-2013

Slide 9: Turkey & CEE banking penetration benchmarks, 2013

Slide 10: Number of banks and banking assets by owner group, 2014 H1

Slide 11: Banking assets evolution (LCU, EUR), 2010-2014 H1

Slide 12: Banking assets evolution by groups of banks, 2010-2014 H1

Slide 13: Top 10 banks, market shares, ownership, 2014 H1

Slide 14: Market concentration, 2014 H1 (Assets, Branches, ATMs, HH Index)

Slide 15: Evolution of market shares for top 5 banks, 2010-2014 H1

Slide 16: Number of bank branches and employment at banks, 2010-2014 H1

Slide 17: Payment infrastructure (ATMs, POS terminals, Cards), 2010-2014 H1

Slide 18: Payment infrastructure (ATM, POS per capita): Turkey vs. Europe, 2013

3. Retail & corporate banking Slide 19: Loans by customer segment evolution, 2010-2014 H1

Slide 20: Deposits by customer segment evolution, 2010-2014 H1

Slide 21: Retail deposits by currency, by maturity, 2010-2014 H1

Slide 22: Concentration of retail deposits by size, 2014 H1

Slide 23: Retail loans by type, 2010-2014 H1

Slide 24: Non-performing loans, ratios by type of product, 2010-2014 H1

Slide 25: Housing loans statistics, 2010-2014 H1

Slide 26: Housing loans - international benchmarking, 2013

4. Banks' profitability Slide 27: Banks - revenue, costs and profits composition, 2013

Slide 28: Banks - profitability tree, 2011-2014 H1

5. Top 5 banks Slide 29: Top Banks (1/5) Turkiye Cumhuriyeti Ziraat Bankasi A.Ş.

Slide 30: Top Banks (2/5) Turkiye Is Bankasi A.Ş.

Slide 31: Top Banks (3/5) Turkiye Garanti Bankasi A.Ş.

Slide 32: Top Banks (4/5) Akbank T.A.Ş.

Slide 33: Top Banks (5/5) Yapi ve Kredi Bankasi A.Ş.

6. Mid-term forecasts Slide 34: Key retail volumes forecast, 2014-2016

Slide 35: Key corporate volumes forecast, 2014-2016

Slide 36: Banking assets forecast, 2014-2016

7. Notes on methodology

Research Report: "Banking market in Turkey, 2014-2016"

Research Report: "Banking market in Turkey, 2014-2016"