The asset management industry in Poland remains in a fast-growing trend. The total value of assets under management (AuM) exceeded PLN 536 billion (EUR 128 billion) as of June 2015. While all key market segments

have demonstrated positive developments, the growth in assets of investment funds has beaten other product groups. Assets of regulated investment funds topped PLN 230 billion, which corresponds to a 9% growth in the first half of 2015 alone.

Outlook

The asset management industry in Poland is expected to sustain a moderate growth at ~7% p.a. by 2017. In-line with historical trends it is investment fund assets, where the fastest growth is expected to occur. Nevertheless also insurance and pension assets are likely

to demonstrate solid performance. A key growth factor will be increasing wealth of individuals thanks to the accelerating economy which supports private wealth formation and emergence of new clients. Today, the asset management industry in Poland is serving directly

over 2 million clients which is a fraction of the population. However, growing disposable income and personal wealth could easily double this figure within the next decade.

2. Asset Management Market

Slide 1: Asset management market in Poland - Key Segments, 2015 H1

Slide 2: Assets under management evolution, 2010-2015 H1

Slide 3: Top asset managers (groups) by AuM, 2015 H1

3. Investment Funds

Slide 4: CEE 7* Investment fund industry - size vs. growth matrix, 2013-2015 H1

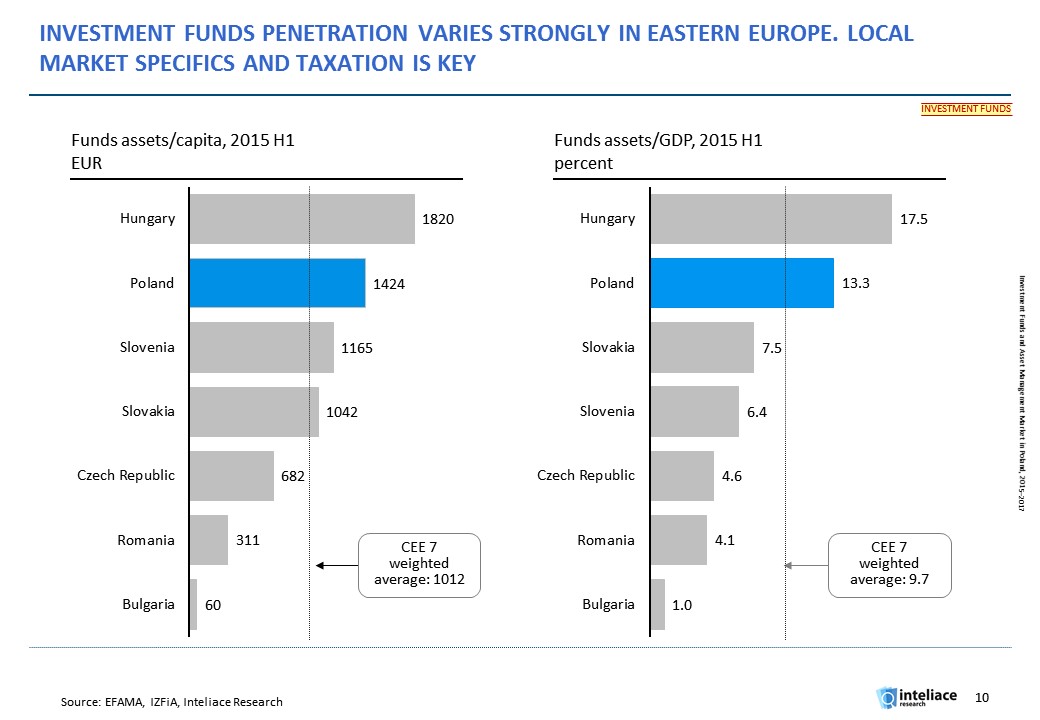

Slide 5: CEE investment funds penetration benchmarks, 2015 H1

Slide 6: Evolution of assets, number of funds & managers 2010-2015 H1

Slide 7: Fund assets by type of fund, 2010–2014

Slide 8: Top players in investment fund market, 2015 H1

Slide 9: Market share evolution of top fund managers, 2011-2015 H1

Slide 10: Distribution channels for investment funds, 2015 H1

Slide 11: Investment fund assets flows, 1Q 2010-2Q 2015

Slide 12: Fund assets structure, 2015 H1

Slide 13: Ownership of funds by groups (retail/financial/other), 2010-2015 Q1

Slide 14: Local funds invested in foreign assets and foreign funds, 2015 H1

Slide 15: Assets of foreign funds, 2010-2015 H1

Slide 16: Fees and commissions charged by top fund managers, 2015 H1

Slide 17: Revenues and costs of fund managers, 2015 H1

Slide 18: Profitability tree for fund managers, 2011-2014

Slide 19: Top players' profiles - PZU TFI

Slide 20: Top players' profiles - Ipopema TFI

Slide 21: Top players' profiles - Pioneer Pekao TFI

Slide 22: Top players' profiles - PKO TFI

Slide 23: Top players' profiles - Skarbiec TFI

Slide 24: M&A transactions including fund managers in Poland (1/2)

Slide 25: M&A transactions including fund managers in Poland (2/2)

Slide 26: Recent case examples of entry of foreign fund managers to Poland

5. Insurance

Slide 33: Insurance assets by type evolution, 2010-2015 H1

Slide 34: Technical reserves by segment and by company, 2014

Slide 35: Profitability of life insurers, 2011-2014

Slide 36: Profitability of non-life insurers, 2011-2014

Investment funds and asset management market in Poland, 2015

Investment funds and asset management market in Poland, 2015