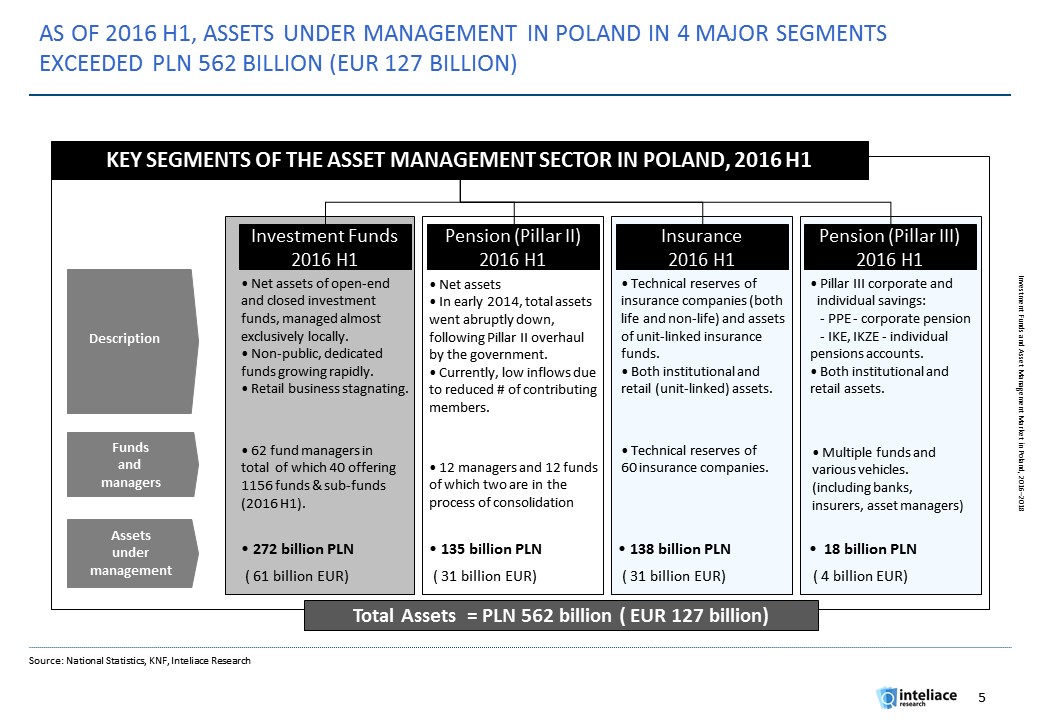

Total assets under management in Poland topped PLN 562 billion or EUR 127 billion across all key categories in H1 2016. The largest part of AM market are investment funds with assets of PLN 272 billion.

Outlook

The asset management sector in Poland is likely to see a further growth in assets under management thanks to increasing households' wealth and corporate savings. Assets are expected to increase across all segments, whereas the highest growth rates could be anticipated in the third pillar pension sector. Although, until recently, most of newly created personal wealth has ended up in investments in productive assets, in banks as deposits or in real estate, future trends are likely to change. Based on historical evidence of more advanced economies, a gradual increase of fund component in savings, could be expected. This will, however, require asset managers to adjust the offer of vehicles and investment strategies to address key issues like: weak local equity market, low efficiency and regulatory developments. Moreover, the current fragmentation in fund management business is unlikely to persist, in view of ongoing consolidation in banking and insurance sectors. Therefore a new wave of consolidation of fund managers is likely to take place. Fund managers will need to increase the scale of operations or they will be forced to quit.

Investment funds and asset management market in Poland, 2016

Investment funds and asset management market in Poland, 2016