After the period of a very fast growth through 2017, total* assets under management in Poland decreased slightly to PLN 629 billion in H1 2019. The recently observed stagnation in total assets could be attributed to the weak performance of the local stock market. The recent correction affected mostly 2nd pillar pension funds, which by law have to overweight equities. Other segments remained relatively stable thanks to new contributions offsetting performance. As of June 2019, assets of regulated investment funds** reached PLN 293 billion, 3rd pillar pension assets exceeded PLN 25 billion and reserves of insurance companies remained almost unchanged at PLN 149*** billion. The asset management market remained medium-concentrated with top four groups: PZU, Aviva, NN and Ipopema managing roughly half of all assets in the market

Outlook

Assets under management in Poland are expected to sustain growth through 2021 while the most action is likely to take place within 3rd pillar pension funds. The new legal framework, in force since mid-2019, has mandated employers to enrol their employees and to match employee contributions. A further boost to 3rd pillar assets could be supplied by the final dismantling of 2nd pillar pension funds, although it would be initially a zero sum game or even a negative event for the sector as a whole

* Across key categories: Investment funds, Insurance assets, Pension assets (2nd and 3rd pillar)

** Funds tracked by IZFiA

*** Technical reserves of non-life and life insurers, including unit-linked life funds

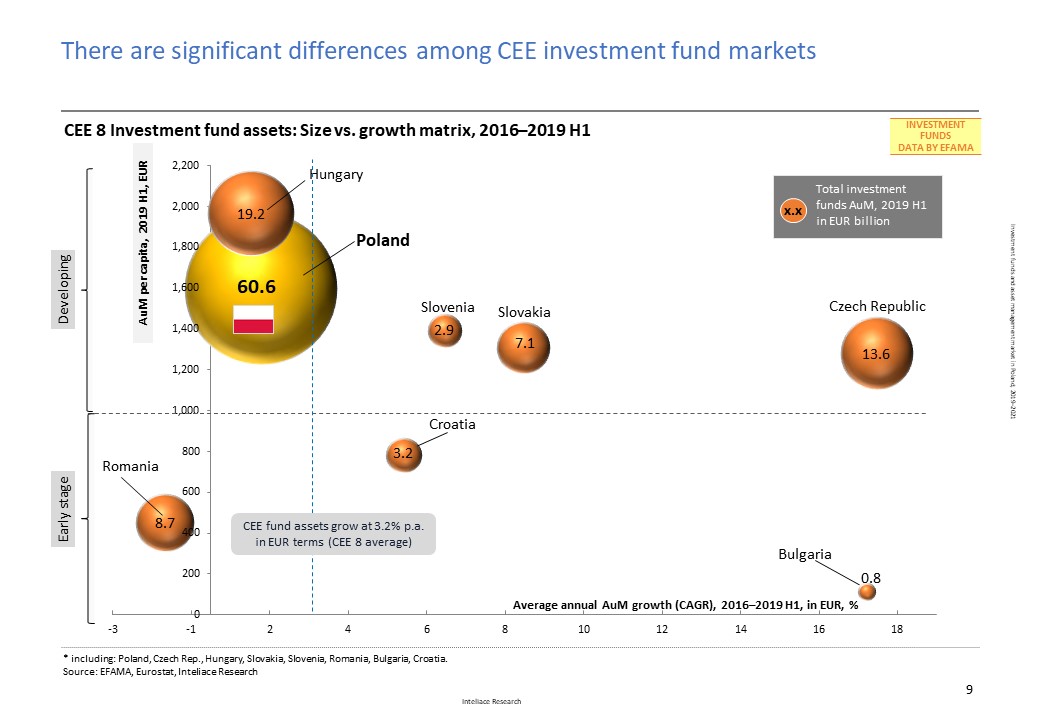

Investment funds and asset management market in Poland, 2019

Investment funds and asset management market in Poland, 2019