Poland's payment market continues to growth rapidly. The total number of payments exceeded 7.5 billion in 2018 and it remained on track to surpass 8.7 billion by 2019. Card payments alone reached nearly 4.7 billion transactions and they accounted for over 62% of all payments processed in the country. The persisting growth in card transactions can be attributed to fast expansion of the acceptance network and to increasing frequency in card use. In 2018, the average annual number of transactions per single card issued in Poland approached 114 tx. per card.

Outlook

The demand for convenient payment services and the ongoing support programs dedicated to the development of acceptance network, e.g. �Cashless Poland�, contribute to a gradual, although slow cash displacement. The current pace of growth in payment volumes is expected to remain strong, similarly to the dominating role of cards in overall payments. As a consequence, the total volume of payments in Poland is likely to reach 12 billion transactions by 2022.

--------------------------------------------------------------------------------------------------------------------------------------

Table of contents

Executive Summary 1. Payments in Poland and in Europe Slide 1: Consumer markets in Europe, 2018

Slide 2: Total payments in Poland, structure by type, 2014-2019F

Slide 3: Total payments: Europe vs. Poland, structure by type, 2018

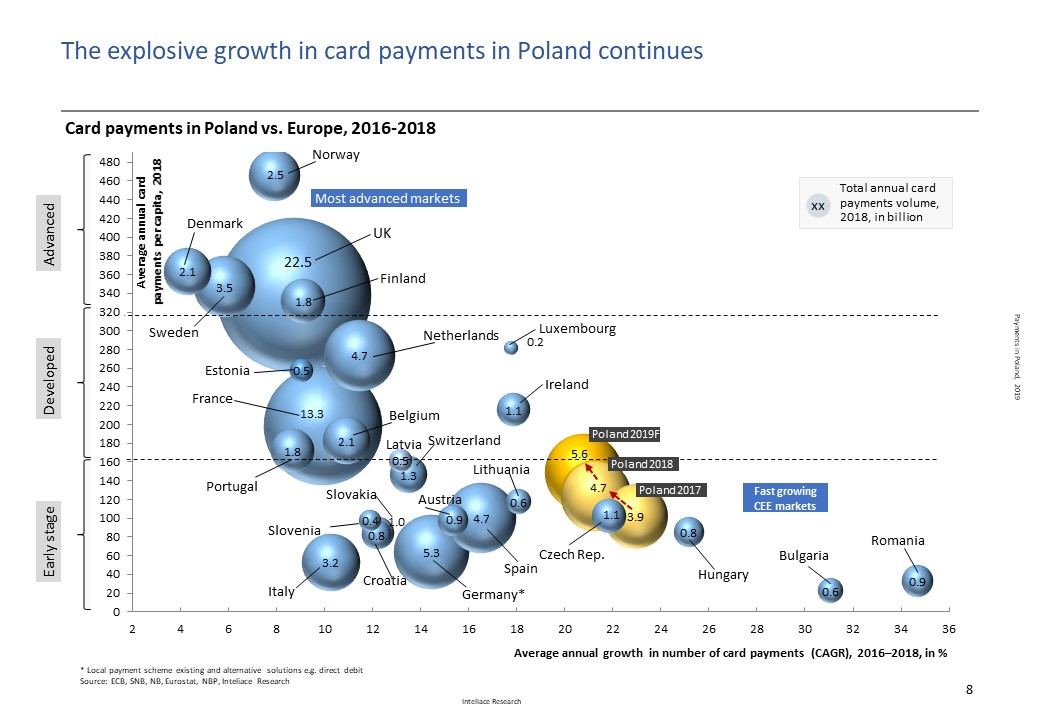

Slide 4: Card payment volumes in Europe & in Poland (1/2), 2016-2018

Slide 5: Card payment volumes in Europe & in Poland (2/2), 2018

2. Payments and payment infrastructure in Poland Slide 6: Card payments in Poland, 2014-2019F

Slide 7: POS infrastructure evolution in Poland, 2014-2019 Q1

Slide 8: Cards/terminals in Poland by functionality, 2015-2019 Q1

Slide 9: ATM networks in Poland, 2014-2019 Q1

Slide 10: ATM cash withdrawals in Poland, 2014-2019F

Slide 11: Cash in circulation and interest rates in Poland, 2012-Aug.2019

Slide 12: Cards issued in Poland, 2014-2019Q1, split by type & brand

Slide 13: Top issuers of payment cards in Poland, 2019 H1

Slide 14: Automated Clearing House (ACH) in Poland; Transaction volumes: ELIXIR, Express ELIXIR, SORBNET2, BlueCash, BLIK, 2012-2018

Slide 15: Evolution of mobile payments in Poland , Global pays

Slide 16: Overview of mobile payments in Poland by origin of funds, 2019

Slide 17: Key players in payment applications/wallets in Poland, 2019

Slide 18: Poland - retail payment services landscape, 2019

Slide 19: HCE-NFC users evolution, key banks in HCE NFC, 2015-2019 Q2

Slide 20: Total payments in Poland, forecast for 2022

3. Retail landscape (merchants) and payment methods Slide 21: Brick&Mortar (physical) vs. online retail, 2018/2019

Slide 22: Key payments methods available in B&M and in online retail, 2019

Slide 23: Survey results summary: Payment methods available in 57 large online stores in Poland, Oct. 2019

Slide 24: Online merchants & payment methods case (1/3): Allegro

Slide 25: Online merchants & payment methods case (2/3): RTVEuroAGD

Slide 26: Online merchants & payment methods case (3/3): empik.com

Slide 27: Key players in specialized mobile payments in public /municipal transportation, 2019

4. Key players by segment Slide 28: Mobile payments, top players and their reach, 2019 Q2

Slide 29: Mobile payments (1/3): BLIK

Slide 30: Mobile payments (2/3): Google Pay

Slide 31: Mobile payments (3/3): Apple Pay

Slide 32: Digital wallets (1/2): MasterPass

Slide 33: Digital wallets (2/2): VISA Checkout

Slide 34: Payment aggregators (1/3): PayU

Slide 35: Payment aggregators (2/3): Przelewy 24

Slide 36: Payment aggregators (3/3): Dotpay/eCard

Slide 37: Digital wallet with hybrid funding: PayPal

Slide 38: Payment gate for ACH-based pay-by-links: Paybynet

Payments in Poland, 2019

Payments in Poland, 2019