In 2013, Poland's GDP growth rate dropped to 1.6% YoY, which was the lowest rate since 2009. Slowing consumer demand and depleting inventories were reducing the GDP growth rate while a healthy growth in exports and a positive balance in foreign trade had a positive contribution. In response to slowing economy, and in-line with global trends, the monetary policy of the Central Bank became looser in 2013 and interest rates were reduced to the lowest levels in modern history of the country. As a consequence of recent economic developments, the insurance sector slowed down with life premium sinking by 14% YoY and non-life premium increasing just by a fraction. The fall in life insurance premium could be attributed almost exclusively to plunging sales of single premium deposit-like products, which became less attractive due to lower interest rates. Other types of saving/investment products, especially unit-linked insurance were unaffected and continued to grow in 2013 reflecting relatively stable financial condition of households and high propensity to save for retirement. Within the non-life business, car insurance suffered from falling premiums (-5% YoY) due to persisting fierce competition among insurers while property, accident and corporate insurance recorded a moderate growth in premiums.

For more information on recent developments in the Polish insurance sector, please refer to the full publication.

Table of contents

Slide 1: Executive summary

1. Macroeconomic overview Slide 2: Poland - General overview

Slide 3: Key macroeconomic indicators, 2007-2013

Slide 4: Foreign trade statistics, C/A, FDI, 2007-2013

Slide 5: Unemployment and wages, 2007-2013

Slide 6: Disposable income in households and income distribution, 2007-2013, (Income distribution 2012)

Slide 7: Consumer confidence index evolution, 2009-Mar. 2014

Slide 8: Warsaw Stock Exchange - Turnover, Market cap. and indexes, 2007-2013

Slide 9: Top 12 foreign investors in banking sector and their subsidiaries, 2013

Slide 10: Banking assets evolution, 2007-2013

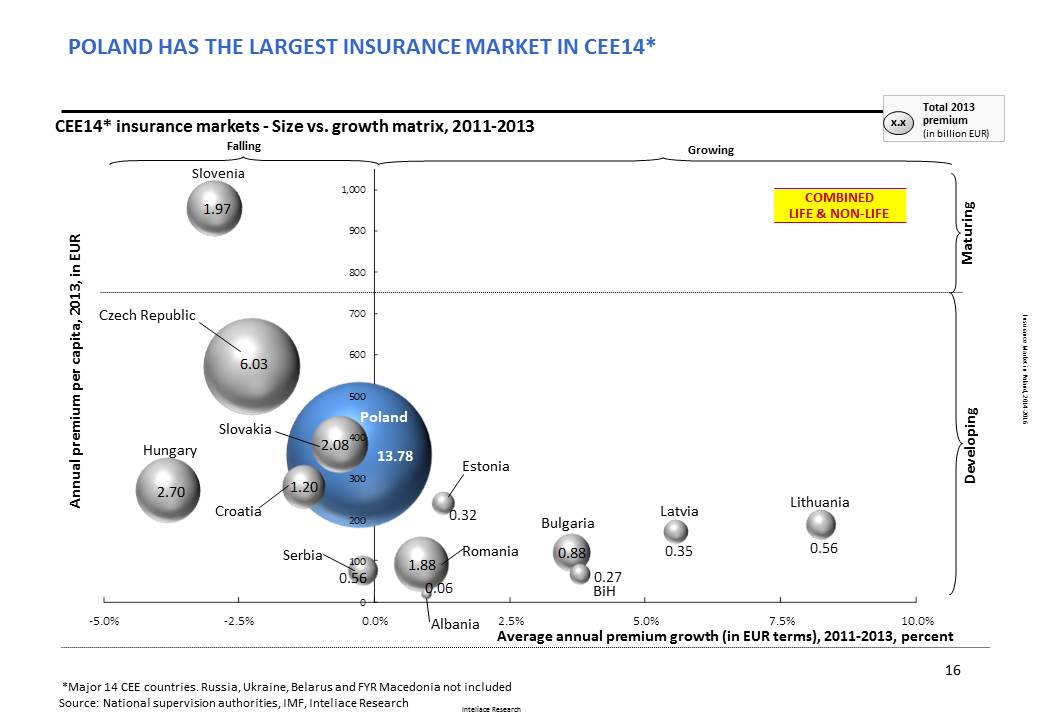

2. Insurance market Slide 11: Insurance Markets in CEE-Size vs. growth matrix, 2011-2013

Slide 12: Insurance premiums per capita & premiums/GDP penetration-CEE comparison, 2013

Slide 13: Insurance gross premiums - Local insurers (life/non-life, in EUR), 2009-2013

Slide 14: Insurance gross premiums - Local insurers (life/non-life, in PLN), 2009-2013

Slide 15: Total premiums collected in Poland (Local + foreign insurers), 2008-2010

Slide 16: Number of locally registered insurance companies, foreign insurers, 2003-2013

Slide 17: Top 12 insurance groups in Poland by total premium written, 2013

Slide 18: Insurance market concentration and Herfindahl-Hirschman Index (life/non-life), 2013-2012

Slide 19: Solvency margin and margin coverage with own funds, 2009-2013

Slide 20: Number of agents and insurance sales personnel, 2008-2012

Slide 21: Insurance-Regulatory institutions, 2013

Slide 22: Private health Insurance-Opportunity for insurers

3. Non-life insurance Slide 23: Non-life insurance markets in CEE-Size vs. growth matrix, 2011-2013

Slide 24: Non-life premiums per capita & premiums/GDP penetration-CEE comparison, 2013

Slide 25: Non-life insurance gross and net premium evolution, 2009-2013

Slide 26: Top 10 non-life insurance players in Poland, 2013

Slide 27: Market shares of top non-life players evolution, 2011-2013

Slide 28: Number of policies and premiums evolution by segment (retail vs. corporate), 2009-2013

Slide 29: Non-life premium by risk class, 2011-2013

Slide 30: Sales channels of non-life insurance, 2010-2012

Slide 31: Direct insurance-key players overview , 2009-2013

Slide 32: Link4-Leader in direct sales in Poland - company profile, 2003-2013

Slide 33: Liberty Direct-a "premium" direct player

Slide 34: Non-life insurers results, technical and P&L accounts, 2013

Slide 35: Non-life insurance - profitability tree, 2009-2013

Slide 36: Non-life insurance - claims and expense ratio evolution, 2009-2013

Slide 37: Non-life insurance - combined ratio and its elements, 2009-2013

Slide 38: Non-life insurance - acquisition costs evolution, 2011-2013, acquisition costs for top non-life insurers comparison, 2012

Slide 38a: Network multi-agents: Consultia, CUK, Unilink etc.

Slide 39: Car insurance - premiums and no. policies evolution, MTPL, Casco, 2009-2013

Slide 40: Car insurance - top players in MTPL and in Casco, 2011-2013

Slide 41: Car insurance - combined ratio and its elements, MTPL and in Casco, 2011-2013

Slide 42: Car insurance - average premium per policy: retail vs. corporate, 4Q2010-4Q2013

Slide 43: Channels/product innovations: ERGO Hestia "You can drive"

4. Life insurance Slide 44: Life insurance markets in CEE - Size vs. growth matrix, 2011-2013

Slide 45: Life premiums per capita & premiums/GDP penetration - CEE comparison, 2013

Slide 46: Life insurance gross and net premiums evolution, 2009-2013

Slide 47: Top 10 life insurance players in Poland, 2013

Slide 48: Market shares of top life players evolution, 2011-2013

Slide 49: Life premium by risk class evolution, 2011-2013

Slide 50: Life premiums and number of policies by client segment and policy type, 2011-2013

Slide 51: Life insurance technical reserves evolution and structure, 2009-2013

Slide 52: Sales channels of life insurance, separately for individual life and group life, 2011-2012

Slide 53: Life insurers results, Technical and P&L accounts, 2013

Slide 54: Life insurance - profitability tree, 2009-2013

Slide 55: Life insurance - acquisition costs evolution, 2011-2013, acquisition costs for top life insurers comparison, 2012

5. Bancassurance & alternative sales channels Slide 56: Bancassurance: Premium written by bank channel (life/non-life), 2010-2012/2013

Slide 57: Bancassurance: Product/class split in bank channel (life/non-life), 2013

Slide 58: Bancassurance: Investment type life products other than unit-linked, 2010-2013

Slide 59: Banking (own) sales platform: "mBank, SUS - Centrum Ubezpieczeń"

Slide 60: Banking (operated by 3rd party) sales platform: "eurobank ubezpieczenia"

Slide 61: Business-to-business sales platforms: "Butik inwestycyjny" operated by TU Europa

Slide 62: Bancassurance: Comparison websites and online sales sites operated - overview

Slide 63: Comparison websites: "ipolisa"

6. Top players' profiles Slide 64: Non-life insurance: PZU, 2011-2013

Slide 65: Non-life insurance: Warta, 2011-2013

Slide 66: Non-life insurance: Ergo Hestia, 2011-2013

Slide 67: Life Insurance: PZU Zycie, 2011-2013

Slide 68: Life Insurance: Open Life, 2011-2013

Slide 69: Life Insurance: TUnZ Warta, 2011-2013

7. Forecast Slide 70: Non-life insurance premiums forecast, 2014-2016

Slide 71: Life Insurance premiums forecast, 2014-2016

Slide 72: Notes on Methodology

Research Report: Insurance market in Poland, 2014-2016

Research Report: Insurance market in Poland, 2014-2016