Poland's payment market has experienced an explosive growth during recent years. The number of card payments has more than doubled since 2013 and it has exceeded 3 billion by 2016. As consumers embraced card payments, Poland advanced to top six European markets by the number of transactions. The key factor of surging use of cards in Poland are contactless payments.

Outlook

The payment market will continue to expand in future as relatively high share of cash in Poland's economy offers a lot room for growth, in particular within: retail payments, P2P, public transport and public fees & duties. There is a clear opportunity in cash displacement and market participants are likely to address it.

One can expect that over next five years a dominating mobile payment standard for mobile payments will evolve itself. It seems for the moment that the new standard will be based on payment cards rather than on ACH.

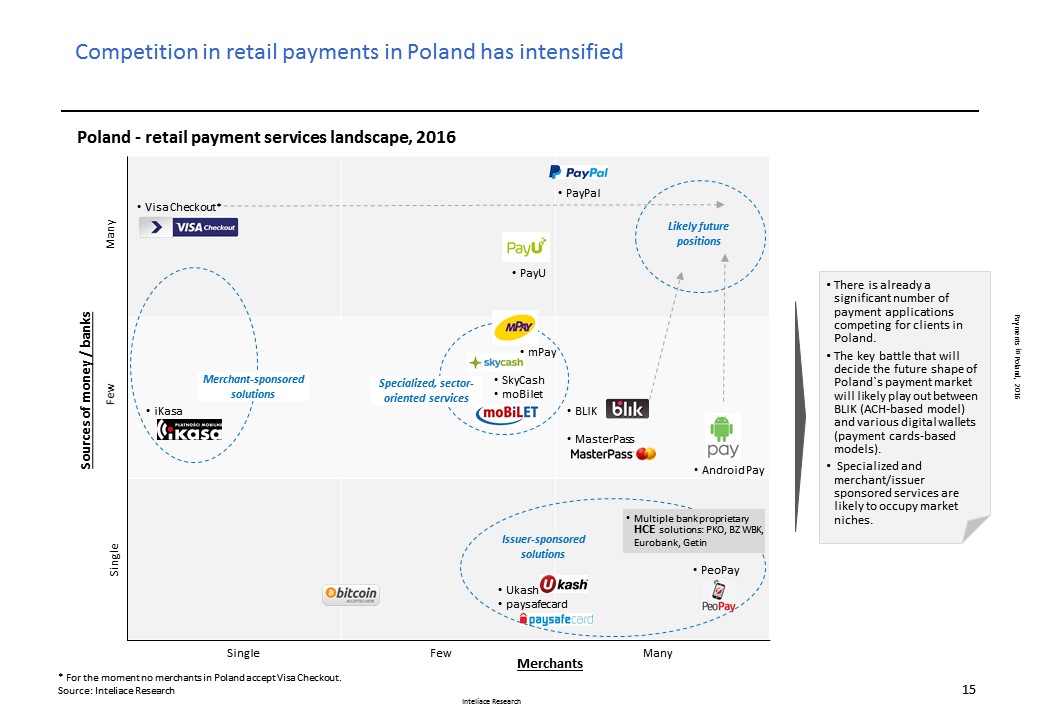

Payments in Poland, 2016

Payments in Poland, 2016