In recent years, the asset management sector in Poland has demonstrated healthy growth, recovering from the contraction observed in 2022. All key market segments* have experienced consistent expansion, leading to a combined total of PLN 907 billion (EUR 214 billion) in assets under management (AuM) by Q2/Q3 2025. Investment funds remain the dominant segment, with AuM of PLN 390 billion, followed by second-pillar pension funds (OFE) at PLN 270 billion and insurance companies’ reserves at PLN 180 billion.

The most dynamic growth has been observed within pension vehicles, particularly the 2nd pillar OFE and PPK. This has been largely an effect of strong equity markets and the significant equity positions taken by these funds. By contrast, investment fund managers (TFI)—which are heavily overweighted with fixed-income instruments—benefited from falling interest rates but could not grow their assets at the same pace as pension products.

Market Leadership and Key Players

Market leadership in the asset management industry is concentrated among a few key players. The top four institutions account for over 55% of the entire market, consistently increasing their combined share year-over-year:

- PZU: Holds the leading position with PLN 187 billion in AuM (22% market share).

- Allianz: Follows with AuM of PLN 112 billion (13% market share).

- Nationale Nederlanden & PKO: Each command approximately 10% of the market.

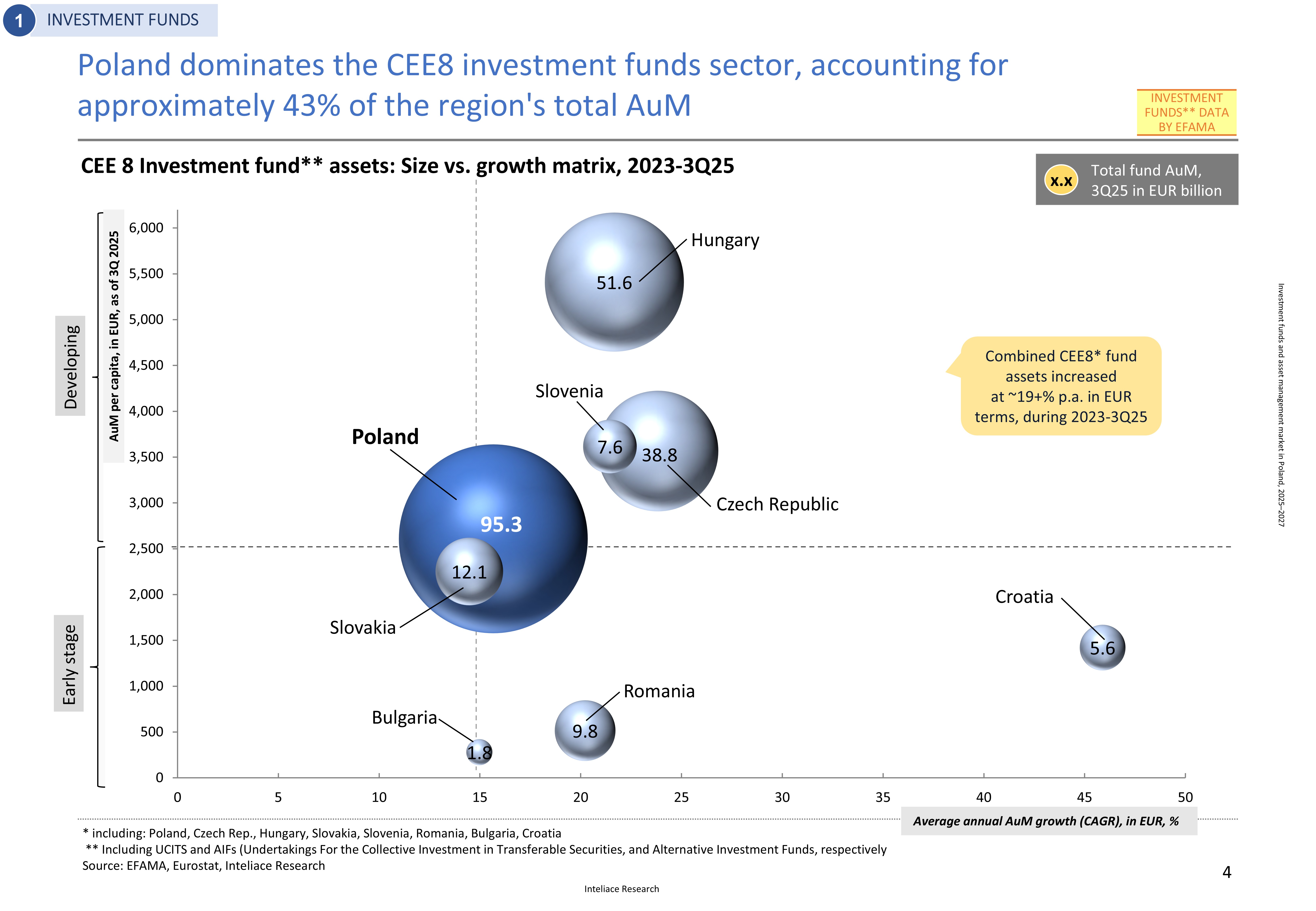

Regional Context and Comparisons

Poland possesses the largest investment funds sector in Central and Eastern Europe (CEE), with over EUR 95 billion in assets under management. Recently, despite the rapid growth of fund assets, Poland's share of the region's total AuM amounted to 43% in Q3 2025.

However, despite maintaining the highest absolute market value, Poland lags behind some of its regional peers in terms of asset value per capita (EUR 2.6k) and assets relative to GDP (11.2%) as of Q3 2025.

The outlook

The asset management market, comprising three main segments—investment funds, insurance reserves, and pension assets—is expected to experience accelerated growth. By December 2027, total assets under management (AuM) are projected to hit nearly PLN 1.2 trillion.

*key categories included: Investment funds, Insurance assets, Pension assets (2nd and 3rd pillar); Excluded are bank and structured deposits, equities, and bonds held directly

--------------------------------------------------------------------------------------------------------------------------------------

Investment funds and asset management market in Poland, 2025

Investment funds and asset management market in Poland, 2025