Research report: Mortgage lending in Poland, 2026

The housing sector exhibited stabilization throughout 2025. Building permits and housing starts declined slightly, while completions continued to increase modestly, reflecting a balanced market adjustment. Residential real estate prices have consolidated since 2024, stabilizing at current levels without significant upward or downward pressure. This price stabilization, combined with the absence of government subsidy programs, has encouraged a more measured approach among developers and buyers alike. The market appears to have reached an equilibrium where supply and demand dynamics support sustainable activity levels without excessive price volatility.

Mortgage lending activity strengthened considerably in Poland in 2025, with new mortgage originations exceeding PLN 103 billion and demonstrating double-digit growth in both value and volume. Despite this robust expansion, the number of active mortgage contracts continues to decline, currently standing at 2.15 million. This contraction reflects ongoing refinancing activity and the systematic closure of legacy foreign-exchange-denominated loans, which have been a persistent challenge for borrowers and lenders alike. The resilience in new lending reflects improved borrower affordability, driven by robust wage growth and tightening labor market conditions.

Poland's mortgage market is positioned for moderate growth through 2028, supported by improving affordability dynamics. Wages are expected to continue rising while residential property prices consolidate, collectively enhancing household purchasing power and lending capacity. In a baseline scenario, outstanding mortgage balances are projected to reach PLN 627 billion by 2028, corresponding to approximately 14% of GDP. This represents accelerated growth of 8% year-over-year, compared to the 5% annual growth observed between 2023 and 2025. However, a significant downside risk exists from potential interest rate increases driven by accelerating global inflation and elevated energy prices. Any such monetary tightening could materially constrain borrowing affordability and dampen the projected expansion of mortgage lending activity.

For more information on recent developments in the Polish banking sector, please refer to the full publication.

Table of contents

Executive summary

1. Residential real estate stock & prices

Slide 1: New dwellings completed, starts, permits, 2010-2025

Slide 2: New dwellings completed by regions, 2025

Slide 3: Residential real estate prices in key cities, 2015-2025

Slide 4: Value and volume of transactions involving real estate, 2018-2024

2. Mortgage lending

Slide 5: Total outstanding lending to households by type of loan, 2021-2025

Slide 6: Mortgage loans to households outstanding, local vs. foreign currency, 2021-2025

Slide 7: Mortgage lending penetration benchmarks - International comparison, 2025 Q3

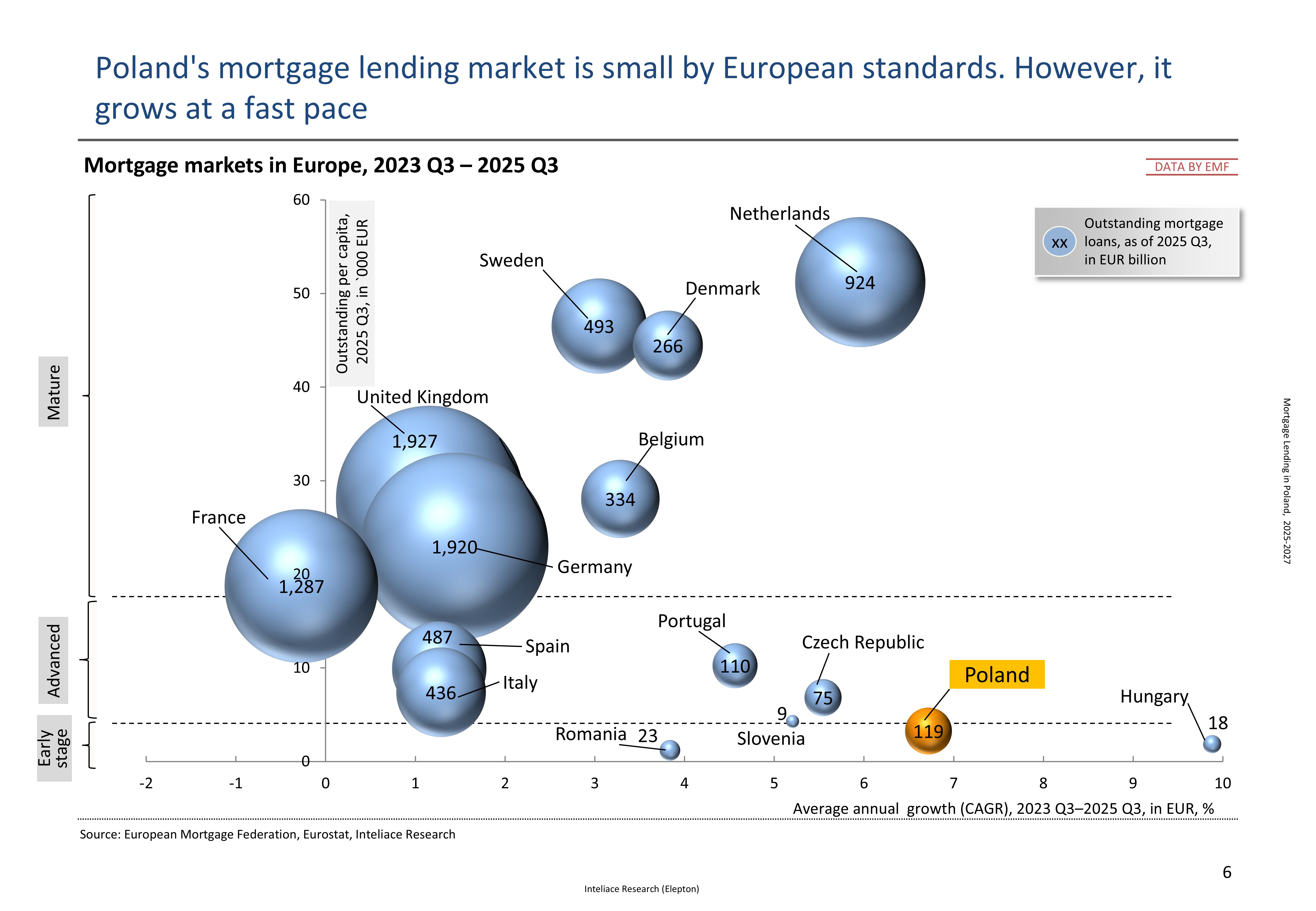

Slide 8: Mortgage lending in Poland vs. Europe- market size vs. growth, 2023-2025 Q3

Slide 9: Number of new mortgage loans, value of new loans, average new loan size, 2021-2025

Slide 10: New sales of mortgage loans to individuals, monthly/annual averages: 2019-Dec.2025

Slide 11: New mortgage loans by size, and by LTV, 2020 - 2025

Slide 12: Top banks by outstanding mortgage loans, 2025 vs. 2024

Slide 13: New mortgage contracts - split by type of interest rate applied (fixed ARM vs. variable), 2022 - 2025

Slide 14: Average lending margins evolution – PLN loans, 2023-2025

Slide 15: The evolution of mortgage loan NPLs, 2022-2025

3. Forecast

Slide 16: Mortgage loans – outstanding value forecast (PLN, FX loans), GDP penetration, 2026-2028(F)

Methodological notes

End of report

Research Report: "Mortgage lending in Poland, 2026-2028"

Research Report: "Mortgage lending in Poland, 2026-2028"