Preview →  Bank outlets Monitor in Poland, 2026"

Bank outlets Monitor in Poland, 2026"

Preview → 9 big bank networks in Poland, 2026"

Preview →

Bank outlets in Poland - network shrinkage hits historical low, first signs of rebound

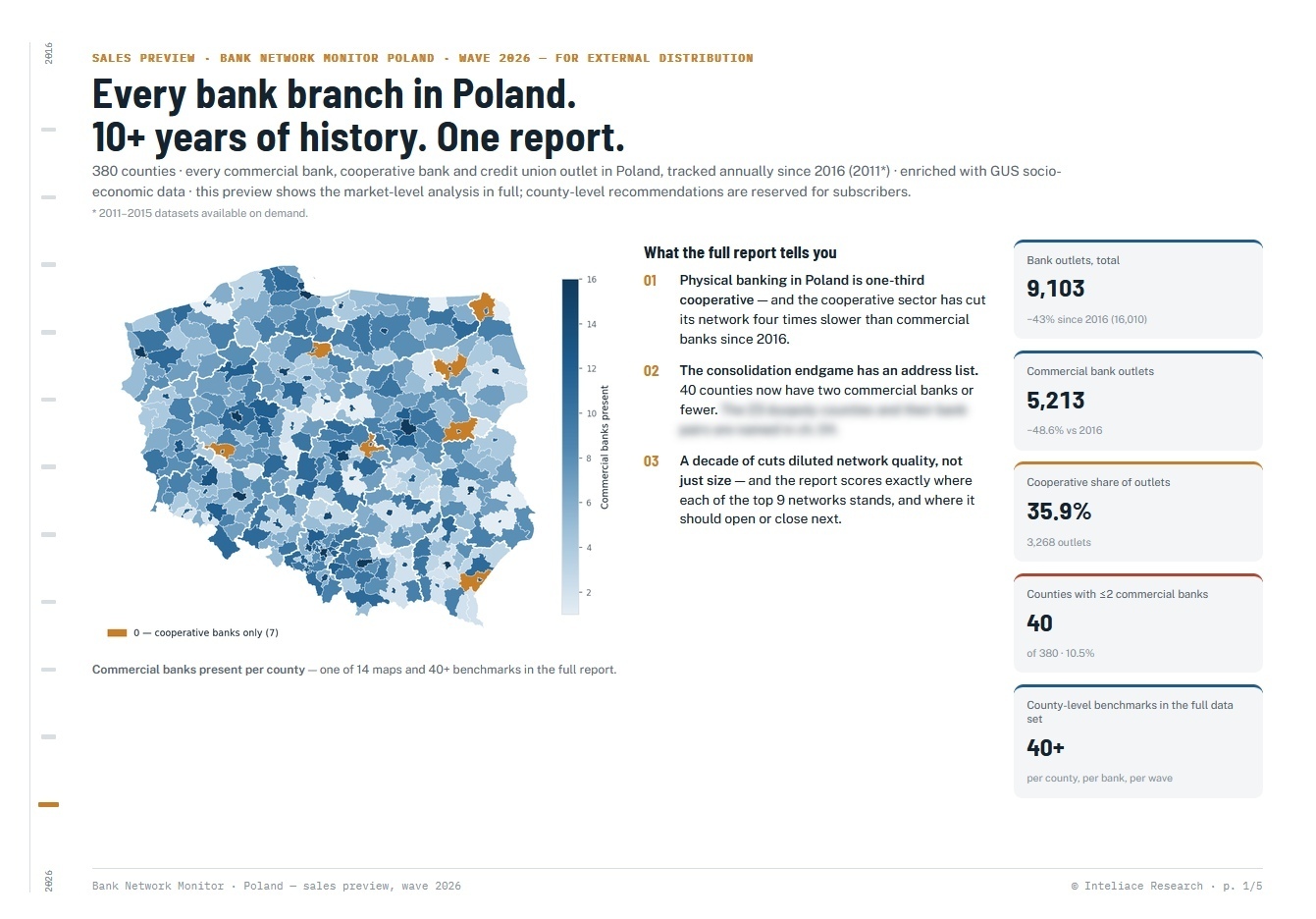

As of April 2026, Poland had a total of 9,103 bank branches. The number declined by 2.0% during the previous 12-month period — the smallest annual contraction recorded in our database. While the long-term trend of network reduction continues, its pace has now slowed for the fourth consecutive year, down from -10.1% at the 2021 peak. This strongly suggests that banks are approaching a minimal viable network size, beyond which further closures would risk eroding customer satisfaction and triggering attrition that outweighs the cost savings from fewer branches.

In the past year, only 184 bank branches were closed in Poland — a marked deceleration compared to over 1,150 closures recorded in 2022 alone. Equally telling is the distribution of change at the local level: out of approximately 380 counties (powiats), 182 recorded no change in branch count, 47 actually gained branches, and only 156 saw a decline — fewer than half. Just four years ago, virtually every county was losing outlets. The map is starting to turn.

Major banking centers continue to host the largest networks, with Warsaw, Kraków, and Wrocław counting 377, 162, and 136 branches respectively. The most notable development of this edition concerns the capital: after nine consecutive years of decline — during which Warsaw's network shrank from 843 to 375 outlets (-55%) — the city recorded its first net gain since 2016, adding 2 branches. In Warsaw, PKO Bank Polski remains the clear leader with 61 outlets (16% market share), followed by Bank Millennium (11%), mBank (10%), and Bank Pekao (10%). Selected mid-sized cities and suburban counties — including Kielce, Gliwice, Siedlce, and the Kraków and Wołomin counties — have also seen modest increases, suggesting that banks are beginning to rebalance their networks toward dynamically growing suburban areas and regional hubs.

The key question is no longer "how fast are banks closing branches?" — it is increasingly becoming "where should branches be located, and what role should they play?" The challenge for 2026 and beyond is no longer retreat, but the active management of an evolving network.

That is exactly the question raw branch counts cannot answer — and exactly what our research is built to answer.

One product, two ways to use it

Bank Network Monitor Poland — Edition 2026 is a single subscription with two complementary components:

📊 The Bank Network Monitor — the full market picture. 380 counties scored on competitive intensity, demand potential, and network saturation; the complete 2016–2026 restructuring story, including the deceleration and county-level turnaround documented above; the local-leader and challenger maps behind numbers like PKO BP's 16% Warsaw share; and the opportunity framework that flags exactly which counties — like the suburban and mid-sized markets named above — are underbanked and primed for expansion.

📋 The Bank One-Pagers — the same analysis, distilled to a single page per network, for each of the 9 major banks (PKO BP, Pekao, Erste/Santander, Millennium, Alior, Credit Agricole, BNP Paribas, mBank, ING BSK). Each card scores where a bank's network actually stands — footprint quality, retail-account productivity, and network-to-market alignment — and names the specific counties it should open, defend, or trim next, with the screening rules shown.

Together they turn "Warsaw added 2 branches" into "here is precisely which bank is winning that shift, why, and where the next one will happen."

See it for yourself

Both components are previewed in full below — real market-level figures and methodology, with the county-by-county and bank-by-bank detail reserved for subscribers:

Bank Network Monitor — preview → ![]() Bank outlets Monitor in Poland, 2026"

Bank outlets Monitor in Poland, 2026"

Bank One-Pagers — preview → ![]() 9 big bank networks in Poland, 2026"

For pricing and the full county-level edition, call us or email us at: info@elepton.pl

9 big bank networks in Poland, 2026"

For pricing and the full county-level edition, call us or email us at: info@elepton.pl

End of report.