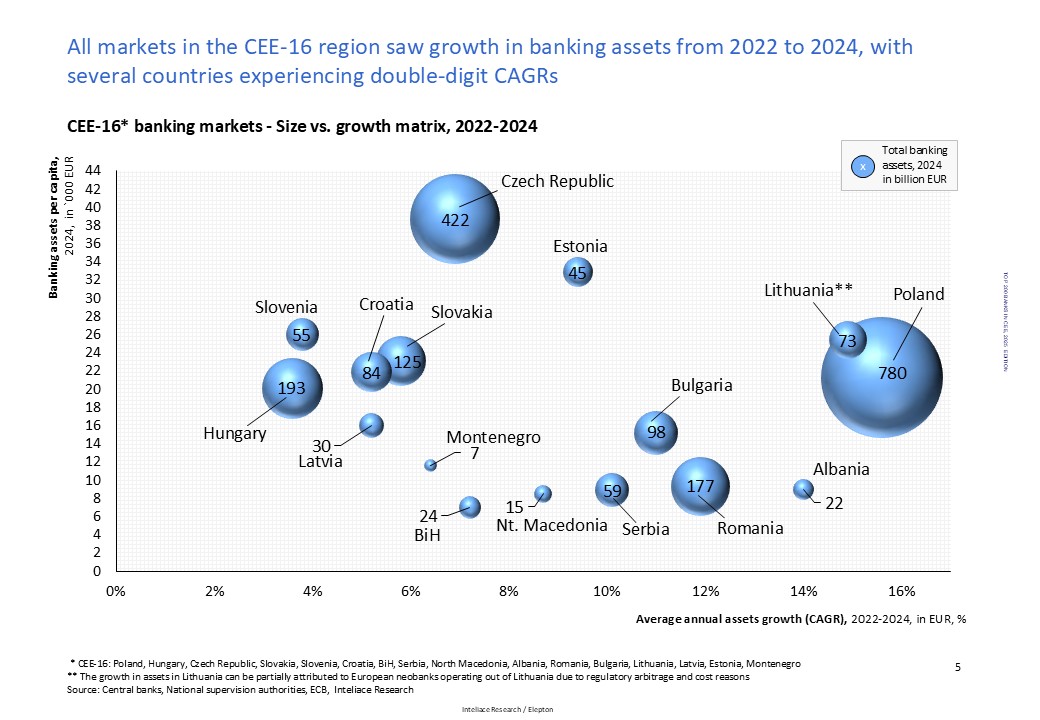

Total banking assets in the CEE16* region reached a record high of EUR 2.2 trillion by December 2024, reflecting an annual increase of 8.3%. This sustained expansion underscores the continued momentum of the Central and Eastern European banking sector, with nearly all 16 countries contributing positively to growth. Notably, Lithuania, Albania, and Poland stood out with annual growth rates exceeding 12%, highlighting the universal strength of the region’s financial ecosystem.

Following a challenging 2020, the sector has not only recovered but has entered a phase of strong profitability. In 2024, the average Return on Equity (ROE) for CEE banks rose to 15.6%, while Return on Assets (ROA) reached 1.56% — both at historic highs. These improvements reflect not only favorable economic conditions but also successful operational optimization.

At the same time, consolidation in the CEE banking sector has accelerated, with leading groups strengthening their positions. A key development in early 2025 was Erste Bank’s acquisition of Santander’s Polish operations — a strategic move that completed Erste’s coverage of Central Europe and elevated its regional market share to 10.7%, with assets exceeding EUR 236 billion. Other major players such as KBC, UniCredit, PKO Bank Polski, OTP, and Raiffeisen also maintain significant regional footprints, with the top 10 groups now controlling EUR 1.2 trillion in assets, accounting for 53% of the market.

These trends indicate a sector characterized by strong fundamentals, growing scale, and increasing sophistication. With continued economic growth and rising demand for banking services, total regional banking assets are expected to exceed EUR 2.5 trillion by 2026.

For more insights, please consult the full report.

------------------------------------------------------------------

*CEE16 include: Poland, Czech Republic, Hungary, Slovak Republic, Romania, Bulgaria, Estonia, Latvia, Lithuania, Croatia, Slovenia, Serbia, Bosnia and Herzegovina, Albania, Montenegro and North Macedonia.

List of Top 200 banks in Central and Eastern Europe /2025 edition/

List of Top 200 banks in Central and Eastern Europe /2025 edition/